Credit Card

IndiaLends App is available in

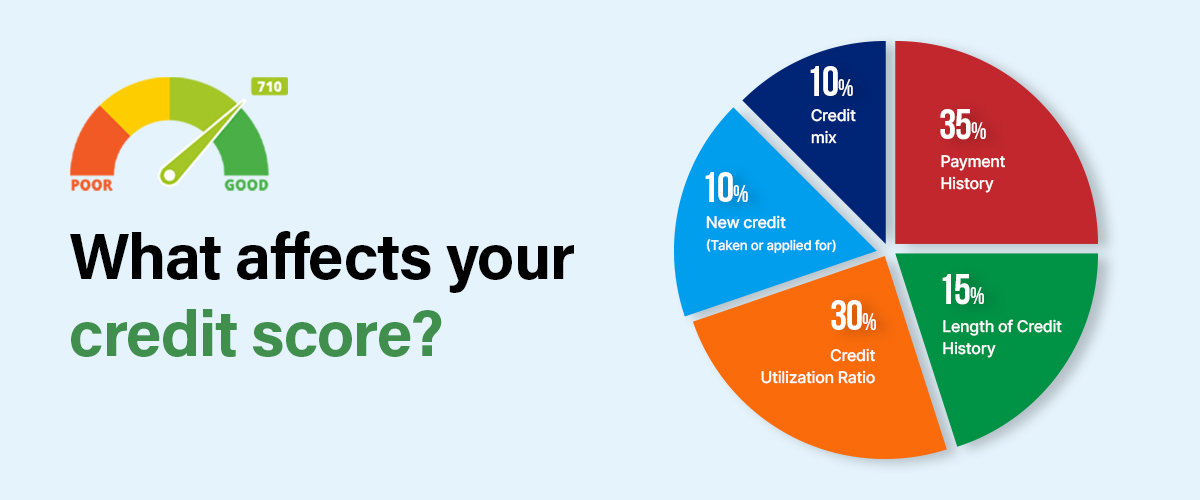

How is your CIBIL score calculated?

Your CIBIL score, often referred to as a credit score, plays a crucial role in determining your creditworthiness. Whether you're applying for a credit card or a personal loan, financial institutions and banks check this three-digit number to assess your credit risk. But have you ever wondered how this score is calculated? Let's understand the components of CIBIL score calculation.

Payment History (35%):

The most significant factor influencing your CIBIL score is your payment history. Timely payment of credit card bills, loan EMIs, and other credit obligations positively impact your score, while late payments, defaults, or bankruptcies can have adverse effects.

Credit Utilisation (30%):

Credit utilization indicates how much of your total credit limit have you used. Maintaining a low credit utilisation ratio is crucial, as it signals responsible credit management. High credit utilisation can indicate financial strain and negatively impact your score.

Length of Credit History (15%):

The duration for which you have held credit accounts contributes to your score. A longer credit history is generally viewed favorably, as it provides a more comprehensive picture of your financial behavior.

Types of Credit in Use (10%):

The variety of credit accounts you hold influences your score. A mix of credit types, such as credit cards and instalment loans, can have a positive impact. However, too many credit inquiries or opening multiple accounts in a short span may raise concerns.

New Credit (10%):

Opening new credit accounts and recent credit inquiries are factored into your score. Too many credit inquiries in just a short span of time can be perceived as a sign of financial distress and may negatively affect your CIBIL score.

If you want to understand “What happens when you apply for multiple cards/loans simultaneously?” read the article here à https://indialends.com/blogs/apply-for-multiple-cards-loans-simultaneously

Pay Bills on Time:

Ensure timely payments for all your credit obligations to maintain a positive payment history.

If you want to know more about credit card default, read the article here à https://indialends.com/blogs/credit-card-default

Manage Credit Utilization:

Aim to keep your credit card balances below 30% of the entire credit limit to maintain a healthy credit utilisation ratio.

Maintain a Mix of Credit Types:

Diversify your credit portfolio by holding a mix of credit types, demonstrating your ability to manage different financial responsibilities.

Avoid Frequent Credit Inquiries:

Limit the number of times you apply for new credit, as multiple inquiries within a short timeframe can impact your CIBIL score.

By focusing on responsible credit management, timely payments, and maintaining a diverse credit portfolio, you can work towards improving and maintaining a good credit score. Regularly checking your credit report for accuracy and addressing any discrepancies promptly is also a crucial aspect of managing your creditworthiness. Remember, a good CIBIL score opens doors to better financial opportunities and terms.

Scan this QR Code

Latest Articles

Common CIBIL Score Myths That Most People Believe

14 May 2026

How Long Does It Take to Improve a CIBIL Score?

14 May 2026

CIBIL vs Experian vs Equifax vs CRIF

13 May 2026

How to Check Your CIBIL Score for Free in India

13 May 2026

Why Loan Applications Get Rejected

13 May 2026

Relevant Articles

How to Reduce Personal Loan EMI Quickly

29 Aug 2025

Credit Card Annual Fee Waiver Tricks

29 Aug 2025

Latest RBI Rules for Personal Loans 2025

29 Aug 2025

How to Get a Personal Loan with a Low CIBIL Score – A Complete Guide by IndiaLends

24 Jul 2025

Things You Didn’t Know Affect Your Credit Score

25 Jun 2025

FAQ’s

Loan against mutual funds (LAMF) allows you to borrow cash against your mutual fund investments as collateral. You can use Volt Money to lien mark your mutual funds digitally to avail an instant limit without losing the ownership of your mutual funds and all the associated benefits with it. Funds will be made available in the form of an overdraft facility.

The annual fee for the Axis Privilege Card is typically Rs. 1,500 plus taxes. This fee can be waived if the cardholder achieves an annual spending milestone, though the exact spending amount for the waiver can vary by card variant. For example, a common waiver condition is spending above Rs. 2.5 lakh in an anniversary year.

Luxe Vouchers are digital gift cards that can be redeemed across popular luxury and lifestyle brands such as Myntra, Flipkart, Pantaloons, and more. Once you qualify for the offer, the voucher code will be sent directly to your registered email ID or mobile number. In most cases, vouchers are delivered within 5–7 working days after successful validation of your transaction or application.

Yes, you can apply even with a low CIBIL score, but your chances of approval may be limited. Most banks and lenders prefer a CIBIL score of 750 or above for quick approval and better interest rates. If your score is lower, some lenders may still consider your application based on other factors such as your income, employment stability, or existing relationship with the bank. However, you may be offered a lower loan amount or higher interest rate. Improving your credit score before applying can increase your chances of getting approved on favorable terms.

URL copied to clipboard successfully !

URL copied to clipboard successfully !Download the IndiaLends App Now

Scan this QR code to download the app