Credit Card

IndiaLends App is available in

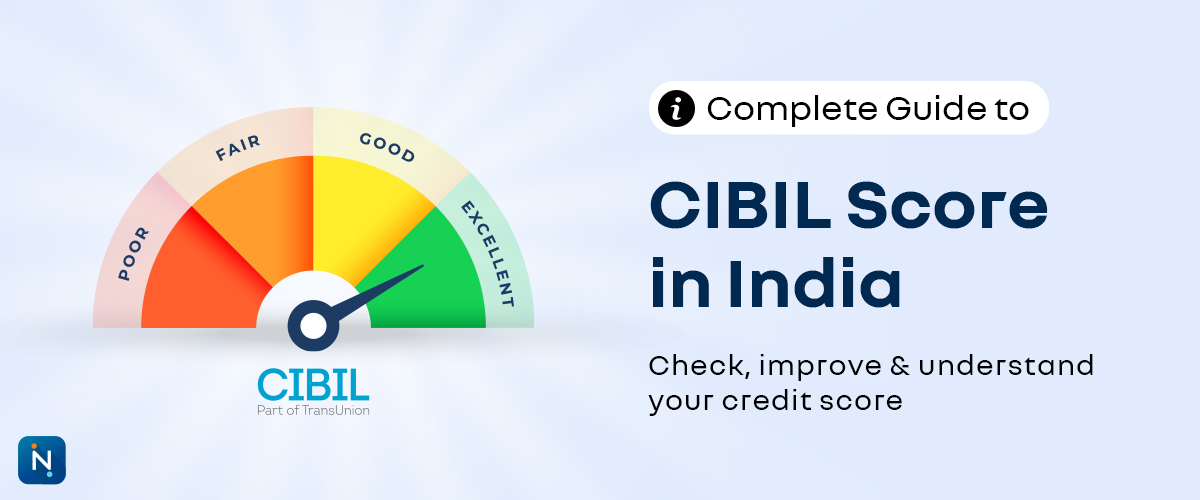

Complete Guide to CIBIL Score in India

Your CIBIL score is one of the most important numbers in your financial life. This 3-digit score influences whether your loan gets approved, the interest rate you are offered, and the type of credit cards you qualify for.

Whether you want to apply for a personal loan, home loan, car loan, or a premium credit card, lenders use your CIBIL score as the first filter. A strong score gives you better borrowing power, while a weak score can lead to rejection or costly loan terms.

This complete guide explains what a CIBIL score is, how it is calculated, how to check it for free, and what steps you can take to improve it in 2026.

What is a CIBIL Score?

A CIBIL score is a 3-digit number ranging from 300 to 900 that represents your creditworthiness. It is calculated by TransUnion CIBIL based on your repayment history, credit usage, and overall credit behaviour.

Every time you use a credit card, repay a loan, miss an EMI, or apply for new credit, that information contributes to your credit report and affects your score. In India, CIBIL is the most widely referenced credit bureau by banks and NBFCs.

Who Are the Credit Bureaus in India?

All four credit bureaus in India are licensed and regulated under the Credit Information Companies Regulation Act, 2005.

CIBIL Score Range Explained

| Score Range | Meaning |

|---|---|

| 300–549 | Poor – high risk to lenders, approvals are difficult |

| 550–649 | Below Average – some lenders may approve, often at higher rates |

| 650–749 | Good – acceptable for many lenders |

| 750–900 | Excellent – best loan offers, faster approvals, better interest rates |

If your score is 750 or above, you are generally in the strongest position to get the best loan and credit card offers.

How is a CIBIL Score Calculated?

Why Your CIBIL Score Matters for Every Loan

How to Check Your CIBIL Score for Free

You can check your CIBIL score for free by visiting the official credit score page and completing a simple verification process.

Check Your Free CIBIL Score Now

Checking your own score is a soft inquiry and does not reduce your CIBIL score.

How to Improve Your CIBIL Score

Common CIBIL Score Mistakes to Avoid

How to Fix Errors in Your CIBIL Report

If your credit report shows inaccurate late payments, duplicate accounts, or loans you never took, you should raise a dispute with the credit bureau immediately.

Ideal CIBIL Score for Different Loans

Conclusion

Your CIBIL score affects almost every major borrowing decision you make. Understanding how it works, checking it regularly, and improving it with consistent habits can help you unlock better loan approvals, lower interest rates, and stronger financial flexibility.

Scan this QR Code

Latest Articles

Common CIBIL Score Myths That Most People Believe

14 May 2026

How Long Does It Take to Improve a CIBIL Score?

14 May 2026

CIBIL vs Experian vs Equifax vs CRIF

13 May 2026

How to Check Your CIBIL Score for Free in India

13 May 2026

Why Loan Applications Get Rejected

13 May 2026

Relevant Articles

Common CIBIL Score Myths That Most People Believe

14 May 2026

How Long Does It Take to Improve a CIBIL Score?

14 May 2026

CIBIL vs Experian vs Equifax vs CRIF

13 May 2026

How to Check Your CIBIL Score for Free in India

13 May 2026

Why Loan Applications Get Rejected

13 May 2026

FAQ’s

A CIBIL score of 750 or above is generally considered excellent in India. It improves your chances of loan approval, better interest rates, and access to premium credit cards.

No. Checking your own CIBIL score is a soft inquiry and does not impact your credit score. Only hard inquiries from lenders can temporarily affect it.

You can improve your CIBIL score by paying all dues on time, keeping your credit card utilization low, avoiding repeated loan applications, and correcting errors in your credit report.

Yes, but approval may be harder and the interest rate may be higher. Traditional banks generally prefer higher scores, while some NBFCs may consider lower-score applicants.

It is a good idea to check your CIBIL score at least once every three months, especially before applying for a loan, credit card, or major financial product.

URL copied to clipboard successfully !

URL copied to clipboard successfully !Download the IndiaLends App Now

Scan this QR code to download the app