Credit Card

IndiaLends App is available in

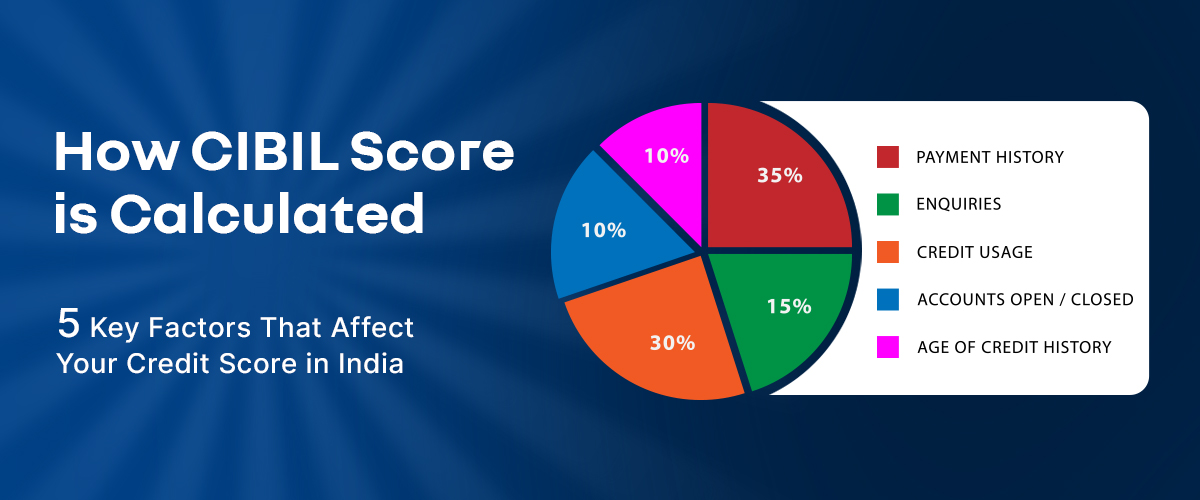

How CIBIL Score is Calculated

Many people know their CIBIL score number but do not fully understand how it is calculated. This matters because if you do not know what drives your score, it becomes difficult to improve it in a strategic and sustainable way.

Your CIBIL score is not random. It is calculated using a weighted model that studies different aspects of your credit behaviour, including repayment habits, credit utilization, credit history length, and recent credit activity.

This guide explains the 5 key factors that affect your CIBIL score in India and what you can do to manage each one better.

Overview: How CIBIL Calculates Your Score

CIBIL collects data from your lenders every month and compiles it into your Credit Information Report. A proprietary algorithm then analyses that data across five major factors and assigns a score between 300 and 900.

Factor 1: Payment History

Payment history is the most important factor in your CIBIL score calculation. It reflects whether you have paid your loan EMIs and credit card bills on time, late, or not at all.

| Payment Behaviour | Impact on CIBIL Score |

|---|---|

| On-time payments | Positive impact over time |

| 30 days late | Moderate negative impact |

| 60 days late | Significant negative impact |

| 90+ days late / default / write-off | Severe and lasting negative impact |

| Settled account | Negative impact |

Even a single missed payment can lower your CIBIL score significantly. Consistent on-time payments remain the strongest lever for improving credit health.

Factor 2: Credit Utilization Ratio

Credit utilization ratio is the percentage of your available credit limit that you are currently using. It is one of the biggest drivers of your CIBIL score after payment history.

| Utilization Level | Score Impact |

|---|---|

| Below 10% | Excellent |

| 10% to 30% | Good |

| 30% to 50% | Fair |

| Above 50% | Poor |

| Near 100% | Very poor, signals financial stress |

The ideal rule is to keep your credit utilization below 30%. Lower utilization signals better control over borrowed money and can support a stronger score.

Factor 3: Length of Credit History

Length of credit history measures how long you have been using credit. CIBIL considers the age of your oldest account, newest account, and the average age of all active accounts.

A longer and stable credit history generally works in your favor because lenders have more data to evaluate your repayment behaviour.

Factor 4: Credit Mix

Credit mix refers to the variety of credit products in your portfolio, such as secured loans, unsecured loans, and credit cards. A balanced mix shows that you can manage different types of borrowing responsibly.

You should not take unnecessary loans only to improve credit mix, but maintaining a naturally diverse portfolio over time can help.

Factor 5: New Credit Inquiries

A new credit inquiry happens whenever a lender checks your CIBIL report after you apply for a loan or credit card. These are called hard inquiries and can temporarily reduce your score.

| Inquiry Type | Meaning | Impact |

|---|---|---|

| Hard Inquiry | Lender checks your report after a credit application | Can reduce your score temporarily |

| Soft Inquiry | You check your own score or a platform does a pre-check | No impact on score |

Applying to multiple lenders in a short period can create several hard inquiries, which may signal credit hunger and reduce your score.

What is Not Included in Your CIBIL Score?

Many people assume salary, savings, or assets directly affect their CIBIL score. They do not. Your CIBIL score focuses on credit behaviour, not overall wealth.

Check Your CIBIL Score and See What is Affecting It

A free credit report helps you understand which factors are helping your score and which ones need immediate attention.

Check Your Free CIBIL Score Now

Conclusion

Once you understand how CIBIL score is calculated, improving it becomes more practical. Focus on timely payments, low credit utilization, a stable credit history, and careful credit applications. Over time, these habits can strengthen your score and improve your borrowing power.

Scan this QR Code

Latest Articles

How to Improve Your CIBIL Score Quickly

23 Apr 2026

CIBIL Score Range Explained (300–900)

07 Apr 2026

What is CIBIL Score?

31 Mar 2026

Complete Guide to CIBIL Score in India

30 Mar 2026

Complete Guide to CIBIL Score in India (2026) | Check, Improve & Boost Your Credit Score

20 Mar 2026

Relevant Articles

How to Improve Your CIBIL Score Quickly

23 Apr 2026

CIBIL Score Range Explained (300–900)

07 Apr 2026

What is CIBIL Score?

31 Mar 2026

Complete Guide to CIBIL Score in India

30 Mar 2026

Complete Guide to CIBIL Score in India (2026) | Check, Improve & Boost Your Credit Score

20 Mar 2026

FAQ’s

Payment history is the most important factor in CIBIL score calculation. It accounts for the biggest share of your score and reflects whether you repay EMIs and credit card bills on time.

Credit utilization affects your CIBIL score by showing how much of your available credit limit you are using. Keeping utilization below 30% is generally recommended for better credit health.

No. Checking your own CIBIL score is treated as a soft inquiry and does not lower your score. Only lender-initiated hard inquiries can have a temporary impact.

CIBIL scores are generally updated monthly after lenders submit fresh repayment and account data. Your score may change each month depending on your latest credit behaviour.

Paying the minimum due helps you avoid a late payment mark, but it does not clear the full balance. Continued high outstanding amounts can keep utilization high and may hurt your score over time.

URL copied to clipboard successfully !

URL copied to clipboard successfully !Download the IndiaLends App Now

Scan this QR code to download the app