Credit Card

IndiaLends App is available in

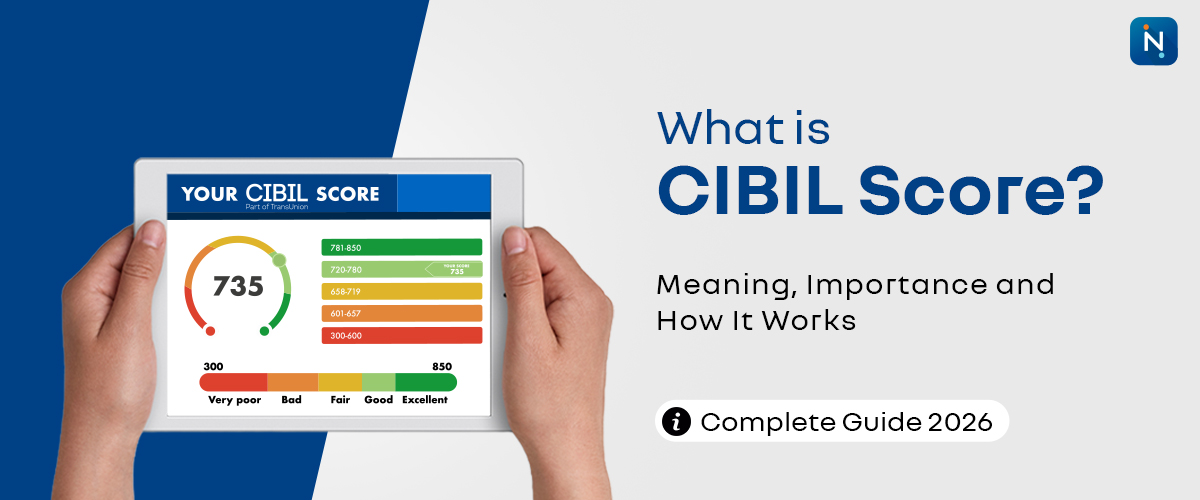

What is CIBIL Score?

You have probably heard the term CIBIL score while applying for a loan or credit card. Banks mention it, lenders ask for it, and many financial products are priced around it. But what exactly is a CIBIL score, and why does it matter so much in India?

This guide explains the meaning of CIBIL score, why it is important, how it works, and how lenders use it to assess your creditworthiness before approving loans and credit cards.

What is a CIBIL Score?

A CIBIL score is a three-digit number between 300 and 900 that represents your creditworthiness. It is calculated by TransUnion CIBIL based on your credit history, repayment behaviour, and overall borrowing pattern over time.

Think of your CIBIL score as your financial report card. Just as academic grades show how a student is performing, your CIBIL score tells lenders how responsibly you handle borrowed money.

What is the Full Form of CIBIL?

CIBIL stands for Credit Information Bureau (India) Limited. It was established in 2000 as India’s first credit bureau and later became TransUnion CIBIL after partnering with global credit reporting company TransUnion.

Who Calculates Your CIBIL Score?

India has four RBI-licensed credit bureaus that generate credit scores:

While all four bureaus issue credit scores, TransUnion CIBIL remains the dominant reference point for most lenders in India.

How Does CIBIL Get Your Financial Data?

CIBIL does not collect your data directly. Banks, NBFCs, and credit card issuers report your credit activity to CIBIL on a monthly basis.

All of this information becomes part of your Credit Information Report, which is then used to calculate your CIBIL score.

Why is CIBIL Score Important in India?

In practical terms, your CIBIL score can directly affect how much you can borrow and how much you will repay over time.

What is a Credit Information Report (CIR)?

Your Credit Information Report, or CIR, is the full report from which your CIBIL score is derived. It contains:

What Does a CIBIL Score of -1 or 0 Mean?

If you have never taken a loan or used a credit card, CIBIL may not have enough data to generate a proper score.

A score of -1 or 0 does not mean your credit is bad. It simply means there is not enough history yet to assess your borrowing behaviour.

Is CIBIL Score the Same as Credit Score?

In everyday usage, people often use the terms CIBIL score and credit score interchangeably. Technically, they are not exactly the same.

Since CIBIL is the most widely used bureau in India, most people refer to credit score as CIBIL score.

Check Your CIBIL Score for Free Right Now

Knowing your score is the first step toward making better financial decisions. It takes less than 2 minutes and is completely free.

Check Your Free CIBIL Score Now

Conclusion

Your CIBIL score is one of the most powerful indicators of your financial credibility in India. Once you understand what it means, how it is calculated, and how lenders use it, you can take better control of your borrowing journey and financial future.

Scan this QR Code

Latest Articles

Common CIBIL Score Myths That Most People Believe

14 May 2026

How Long Does It Take to Improve a CIBIL Score?

14 May 2026

CIBIL vs Experian vs Equifax vs CRIF

13 May 2026

How to Check Your CIBIL Score for Free in India

13 May 2026

Why Loan Applications Get Rejected

13 May 2026

Relevant Articles

Common CIBIL Score Myths That Most People Believe

14 May 2026

How Long Does It Take to Improve a CIBIL Score?

14 May 2026

CIBIL vs Experian vs Equifax vs CRIF

13 May 2026

How to Check Your CIBIL Score for Free in India

13 May 2026

Why Loan Applications Get Rejected

13 May 2026

FAQ’s

A CIBIL score is a three-digit number between 300 and 900 that represents your creditworthiness based on your loan and credit card repayment history. A higher score indicates better credit health.

TransUnion CIBIL calculates the CIBIL score using credit data reported by banks, NBFCs, and credit card companies. It is the most widely used credit bureau in India.

Not exactly. Credit score is a general term, while CIBIL score specifically refers to the score generated by TransUnion CIBIL. In India, both terms are often used interchangeably.

A score of -1 means you have no credit history, while a score of 0 usually means your credit history is too new to generate a valid score. It does not mean you have bad credit.

Your CIBIL score affects loan approvals, interest rates, credit card eligibility, and even how quickly your application is processed. A strong score improves your borrowing power and access to better financial products.

URL copied to clipboard successfully !

URL copied to clipboard successfully !Download the IndiaLends App Now

Scan this QR code to download the app